Nancy Pelosi, former Speaker of the House of Representatives, is known for her political prowess. But she has also gained fame (or notoriety), along with her husband, Paul Pelosi, who runs a San Francisco–based venture capital investment firm, as the investing GOAT (Greatest of All Time). According to Yahoo Finance, citing information provided by the trading platform Autopilot, in 2024, the Pelosi stock portfolio appreciated by a whopping 54%, enough to outperform almost the entire hedge fund universe.

We’ll review five 2025 Pelosi trades, as reported in the latest Periodic Transaction Report, available at November 15, 2025, filed by the Speaker Emerita. Don’t be surprised to run into some of the usual suspects, such as “Magnificent Seven” stocks, plus a couple of names that may be less well-known. You’ll also notice that despite being bullish (thinking the stocks were a good buy), the Pelosis did not buy the stocks in these trades. Yet, the trades were meant to profit if the stock prices went up, just as if the stocks were owned.

Let’s see how it’s possible to benefit from a stock’s price appreciation without actually owning the stock. You can do that by using options, specifically call options. You’ll buy a call option on a stock when you expect the price of that stock to go up, just as the Pelosis did.

Primer on Options

What Is a Call Option on a Stock?

A call option is a contract that gives you the right, but not the obligation, to buy a stock at a specific price, known as the strike or exercise price, before a certain date (the expiration date). You pay a premium upfront for this right. So, while you’re not actually buying the stock, until the option expiry date, you can buy the stock, if you so desire. Also, importantly, you do not have to buy the stock, if you don’t want to.

Three Key Ingredients of a Call Option

1. The Strike Price (Exercise Price)

This is the price you can choose to buy the stock at.

2. The Expiration Date

The deadline. After this date, the option ceases to exist.

3. The Premium

The purchase price of the option.

This is the most you can lose. It’s the amount you’ll lose if the option is not used.

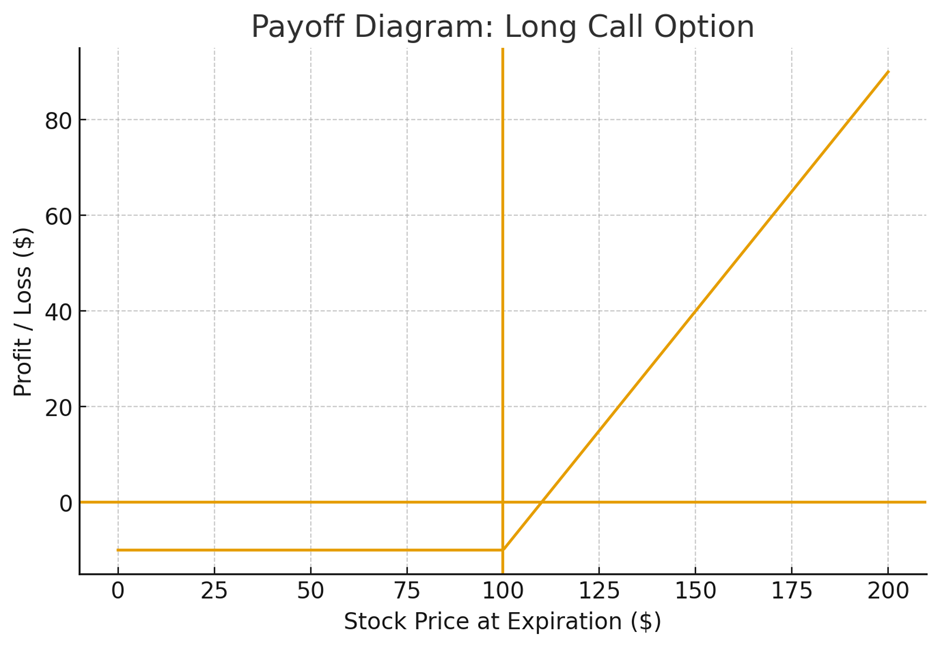

How does a Call Option Work?

You would buy a call option on a stock, if you expect the price of the stock to go up. For example, you purchase an option for $5 with a strike price of $100, because you believe the price will go higher than $100. If the price of the stock never rises above $100, the option is worthless, and you lose $5, the price you paid for the option.

However, if the stock price climbs above $100, you’re in the money. Suppose the price rises to $130. You’ll be able to buy the stock for $100 and sell it in the market for $130, thus realizing a profit of $130 – $100 – $5 = $25.

So, if you buy a call, you’ll get:

- Unlimited upside, plus

- Limited downside: the most you can lose is the premium, i.e. the price of the option.

A call option is a low-cost way to bet the price of a stock will rise, giving you the right but not the obligation to buy that stock at a lower price than the market price before a particular deadline.

In the stock analyses that follow, we reviewed five parameters that a prudent investor might look at when considering whether or not to buy a stock. These are revenue growth, profitability, balance sheet strength, valuation, and competitive advantage.

Nancy’s Five Star Trades in 2025

Alphabet Inc. – Class A Common Stock (GOOGL)

In January 2025, Nancy Pelosi and her husband purchased 50 call options on the Class A Common Stock of Alphabet Inc. (GOOGL). The options had a strike price of $150 and are set to expire on January 16, 1926.

1. Revenue Growth

Alphabet continues to show strong top-line momentum for a company of its size. The firm surpassed $100 billion in quarterly revenue in Q3 2025, growing roughly 16% year-over-year, and this was after 14% growth in Q2. Amazingly, revenue has nearly doubled since 2020, driven not only by search and advertising but also by expanding segments such as cloud computing, AI infrastructure, and subscription services.

2. Profitability

Alphabet’s margins remain impressive. Gross margins have hovered around 60%, and operating and net margins continue to rise. High returns on equity and invested capital, often in the high-20% to 30% range, are signs that the company has an efficient, scalable business model.

3. Balance Sheet Strength

With extremely low leverage (debt-to-equity 0.03) and a strong liquidity profile (current ratio 1.95), Alphabet has one of the strongest balance sheets in large-cap tech. Massive cash generation and a market cap approaching $3 trillion provide resilience against economic or industry slowdowns.

4. Valuation

Valuation is the most debated aspect of Alphabet’s investment case. Some analysts view the stock as overvalued under conservative assumptions, while others argue that a P/E of 22–23× is reasonable given mid-teens revenue growth and expanding margins.

5. Competitive Advantage

Alphabet is widely regarded as having a “wide moat” defense due to its dominance in search, massive data resources, brand strength, and network effects. These structural advantages support long-term durability and high returns.

For Millennials and Gen Z adults, Alphabet represents a blend of long-term stability and exposure to the technologies shaping their future, such as the AI, cloud computing, and digital platforms they use every day. Its strong balance sheet and durable competitive moat make it a fairly safe investment. It’s also a great portfolio compounder. The company does pay a dividend, but most of its profit is reinvested: the reinvestment ratio is about 92%.

Alphabet aligns well with younger investors who favor companies building the digital infrastructure of the next several decades. The only caveat is pricing. At present valuations, it may be highly priced. However, that elevated price may simply reflect that investors are betting its substantial reinvestment translates into higher future earnings.

Amazon.com, Inc. – Common Stock (AMZN)

The Pelosi portfolio also purchased 50 call options of Amazon.com, Inc. Common Stock (AMZN) with a strike price of $150 and an expiration date of January 16, 2026.

1. Revenue Growth

Amazon’s top line continues its upward trend. Revenues rose by 12% from $514 billion in 2022 to $575 billion in 2023, and then by 11% to $638 billion in 2024. That upward trajectory shows no signs of slowing. For the TTM (Trailing Twelve Months) ending September 2025, revenues climbed to $691 billion, a 11.5% year over year increase.

2. Profitability

Profitability appears to be strengthening. In 2024, Amazon generated $68.6 billion in operating income with an operating margin of 10.8%, up from 6% in prior periods. Net margins improved to 7.8% in 2024 and crossed 11% in mid-2025, while gross margins average around 50%.

3. Balance Sheet Strength

Amazon’s financials show substantial operating cash flow, i.e. the cash generated from operations. There’s enough cash on hand to continue funding Amazon’s three main operating areas: logistics, data centers, and AI infrastructure. Free cash flow is rising. As a result, shareholders may soon begin demanding dividend payments or return of capital. Free cash flow is the residual cash available after capital expenditures (CAPEX).

4. Valuation

Amazon’s valuation depends heavily on expectations for AWS, advertising, AI, and long-term efficiencies. The stock commands a premium because it is a large, mature company with structural advantages. Whether it’s “fairly valued” or “expensive” depends on one’s growth assumptions.

5. Competitive Advantage

Amazon’s competitive moat is built on the scale of its retail operations, its unmatched logistic network, a dominant cloud platform, and a rapidly expanding advertising ecosystem. These overlapping advantages create customer stickiness and high switching costs. The company has its fingers in many pies. Amazon’s diversification across retail, cloud, and advertising reduces reliance on any single revenue stream.

For Millennial and GenZ investors, Amazon offers a powerful combination of innovation, diversification, and scalability, similar to the investment in Alphabet. With Amazon, they’ll get exposure to AWS, AI infrastructure, logistics, and digital advertising, as well as the company’s powerhouse retail operation. Rising margins and strengthening cash flow make Amazon attractive for younger investors who want long-duration assets capable of compounding over time, especially in industries tied directly to their lifestyles.

NVIDIA Corporation – Common Stock (NVDA)

The Pelosis purchased 50 call options of NVIDIA Corporation Common Stock (NVDA). The options have a strike price of $80 and an expiration date of January 16, 2026.

1. Revenue Growth

NVIDIA is experiencing extraordinary revenue expansion driven by the global AI infrastructure boom. FY 2025 (year to Jan 2025) revenue surged to $130.5 billion, up 114% from the prior year. The momentum has continued into FY 2026 (year to Jan 2026), with Q1 revenue rising 69% year-over-year and Q2 rising 56% to $46.7 billion. There’s no doubt that revenue growth is NVIDIA’s standout strength and a defining feature of its investment profile.

2. Profitability

NVIDIA combines accelerated growth with healthy profitability. FY 2025 gross margins were 75%, with Q2 FY 2026 maintaining a 72% level. These are margins that hardware companies never achieve. Free-cash-flow margins of 29% underscore how efficiently the company converts revenue into cash. NVIDIA is a money-making machine.

3. Balance Sheet Strength

NVIDIA’s massive cash generation, expanding profit base, and ability to deploy capital into R&D and manufacturing capacity point toward solid financial health. The company operates in a capital-intensive industry, but is able to fund expansion without external financing.

4. Valuation

Here the picture becomes more nuanced. Analysts warn that NVIDIA’s valuation already embeds very high expectations. Slowing growth or decelerating margins could trigger a correction.

5. Competitive Advantage

NVIDIA holds a dominant position in AI hardware, GPUs, and data-center acceleration. This is a position that is strengthened by its Blackwell architecture, its CUDA software ecosystem, deep partnerships with cloud providers, and first-mover scale advantages. These factors create high switching costs and a powerful moat.

To Millennial and Gen-Z investors, NVIDIA represents a pure-play on the AI revolution, a rare chance to invest directly in the hardware and software stack powering everything from gaming to autonomous vehicles to generative AI. Its explosive revenue growth and unique competitive moat make it one of the most compelling long-term innovation plays. While volatility is part of the story, NVIDIA’s role at the center of global AI demand makes it especially meaningful for younger investors building high-growth portfolios.

Tempus AI, Inc. – Class A Common Stock (TEM)

The Pelosis purchased 50 call options of Tempus AI, Inc. Class A Common Stock (TEM), with a strike price of $20 and an expiration date of January 16, 2026.

1. Revenue Growth

Tempus AI is showing exceptionally strong top-line growth. FY 2024 revenue reached $693 million, and by the TTM period ending September 2025 revenue had climbed to $1.1 billion; that’s about 73% year-on-year growth. Q3 2025 revenue grew 85% to $334 million. Growth in the 70–80% range is rare for a public company at this scale and signals that Tempus is gaining traction in its healthcare AI, diagnostics, and data-platform markets. It is clear that revenue growth is one of Tempus AI’s most compelling strengths.

2. Profitability

Despite high gross margins (62%), the company remains unprofitable with a TTM net loss of about $204 million and a negative free-cash-flow margin of roughly 22%. The strong gross margin suggests the underlying business model can be profitable at scale, but current losses reflect heavy investments in R&D, infrastructure, and expansion. For healthcare-professional investors, this means the company is still in a growth-first phase and has not yet demonstrated bottom-line durability. Thus, profitability is currently a weakness, with losses overshadowing revenue momentum.

3. Balance Sheet Strength

Available snapshots show total assets around $2.28 billion and liabilities ranging from $350 million to $1.77 billion depending on the reporting period. While these ratios do not signal obvious distress, negative cash flow means the company must carefully manage spending and fundraising to avoid liquidity pressure. The balance sheet appears adequate but not unequivocally strong.

4. Valuation

Tempus trades at a premium, with a forward price-to-sales ratio above 10×, well above industry norms. Analysts project strong future growth, but the high valuation means investors are paying for anticipated success rather than current profitability. If revenue growth slows or margins decline, Tempus will face challenging times.

5. Competitive Advantage

Tempus has built a sizable multimodal healthcare data platform. The company maintains partnerships across pharma and clinical networks; approximately 3,000 healthcare institutions are connected to its platform. This is a promising foundation; one that is rooted in real clinical utility. However, healthcare data markets face regulatory friction, reimbursement uncertainty, and rising competition. As a result, while Tempus does have competitive advantage, it’s position is not fully secured; execution will determine whether Tempus can build an enduring moat.

Tempus AI will appeal to younger investors who are comfortable with early-stage, high-growth companies operating at the intersection of data, healthcare, and artificial intelligence. While unprofitable today, its rapid revenue growth and expanding data platform provide exposure to the future of precision medicine, an area Millennials and Gen Z often value both financially and socially. For those with long time horizons and higher risk tolerance, Tempus represents a forward-looking opportunity in a transformative sector.

Vistra Corp. Common Stock (VST)

The Pelosis purchased 50 call options of Vistra Corp. Common Stock (VST), with a strike price of $50. The options are set to expire on January 16, 2026.

1. Revenue Growth

Vistra is an electricity and power generation company that’s on a roll. In FY 2024, the company generated $17.2 billion in annual revenues, a figure that represented a 16.5% rise from the prior year’s $14.8 billion. Trailing-twelve-month revenue remains near $17.19 billion. Operationally, Q3 2025 Adjusted EBITDA rose to $1.58 billion from $1.44 billion in the prior year, a development that indicates efficiency is improving. While this level of revenue growth is not explosive, it is strong for a mature energy and utilities company, an industry typically characterized by stable demand and slower expansion.

2. Profitability

Vistra posted $652 million in net income in Q3 2025. Over the TTM period, net income totaled about $960 million, though margins have compressed from 11.4% to 5.6%. A TTM P/E ratio near 63 suggests that earnings are thin relative to valuation, and that the market expects significant future improvement. Low single-digit margins are typical for utilities but expose profits to swings in fuel costs, regulation, and energy prices.

3. Balance Sheet Strength

Vistra reported approximately $3.7 billion in available liquidity (cash plus revolver access to credit) in Q3 2025,an encouraging sign. However, a low solvency score (25/100) and indications of high leverage highlight balance-sheet risk. Utilities often carry substantial debt due to capital-intensive infrastructure, but this still raises concerns about flexibility in downturns or during fuel-price spikes.

4. Valuation

Some analysts assign a 12-month price target implying 33% upside. Yet others characterize the stock as slightly overvalued, and with a P/E above 60, investors are clearly paying a premium. Such valuation is based on expectations of rising electricity demand from AI data centers and broader electrification trends, not on current margins.

5. Competitive Advantage

Vistra is a large integrated energy provider with a diversified generation mix across nuclear, natural gas, solar, coal, and storage. Its scale and recent acquisitions position it to benefit from growing power demand, particularly from AI-driven data-center expansion.

Still, the sector faces regulatory scrutiny, commodity-price exposure, and rapid technological change, all of which complicate long-term competitive durability. Competitive advantage is a moderate strength, real but conditional on execution and industry dynamics. Nevertheless, overall, Vistra offers steady growth, strong sector tailwinds, and strategic positioning, but profitability, leverage, and valuation pose meaningful risks.

For Millennials and Gen Z, Vistra offers something different: exposure to the accelerating electrification of the economy, notably the massive power demands created by AI data centers. While utilities aren’t typically flashy, Vistra sits at the nexus of a structural shift in energy consumption. Younger investors seeking diversification beyond tech may find Vistra attractive because electricity is about to become even more ubiquitous.

Conclusion

Taken together, these five Pelosi trades highlight how sophisticated investors position themselves at the intersection of long-term structural trends that create opportunity. The confluence of developments in AI, cloud computing, digital advertising, healthcare data, and the electrification of the economy have created an entirely new investment landscape.

Whether through mega-cap compounders like Alphabet, Amazon, and NVIDIA or high-growth innovators like Tempus AI and infrastructural plays like Vistra, the underlying theme is the same: opportunities will emerge as technology advances and data management improves.

For younger investors, the lesson here isn’t to mimic any individual trade, but to understand the fundamentals that make these companies compelling in the first place. By focusing on durable growth drivers, strong competitive moats, and future-oriented industries, Millennials and Gen Z can build portfolios that reflect both their financial goals and the world they expect to live in.